Why Tech Stocks Could Stumble Amidst Rising Rates

Prospects for higher interest rates sooner rather than later really appear to be disproportionately whacking Tech stocks. Given that many of these companies retain substantial sums of cash net of debt on their balance sheets, this trading behavior may be confusing to many investors. Institutional investors’ concerns likely focus on the discounted value of Tech companies’ future cash flows rather than on its prospective balance sheet condition.

Prospects for higher interest rates sooner rather than later really appear to be disproportionately whacking Tech stocks. Given that many of these companies retain substantial sums of cash net of debt on their balance sheets, this trading behavior may be confusing to many investors. Institutional investors’ concerns likely focus on the discounted value of Tech companies’ future cash flows rather than on its prospective balance sheet condition.

Theoretically, for a company generating $1 billion in free cash flow with a 7% average cost of capital – its discount rate – incurring a two-percent increase in that discount rate, while relatively benign optically, translates to an estimated reduction in value of $17M+ in a year. If our company has 100M shares outstanding and trades at 20x free cash flow, that $17M drop in value results in a share price decline of only $3.43, or about 1.7%. That price change falls well within the range of typical market gyrations and probably, never garners another thought.

However, that theoretical increase in the company’s discount rate also likely results in a down-tick in the cash flow multiple that investors will pay for shares of the company, say from 20x to 18x. Now, that $17M decline in value amounts to a $23.09, or 11.5%, downward revision in value. Even for the most resilient, longest-term investor an 11.5% price drop likely results in at least a raised eyebrow.

Of course investors may argue that rising rates impact companies across sectors and question why Tech trades differently. Two factors, in our view, serve to explain Tech’s potentially increased sensitivity to rates vis-à-vis companies in other sectors: 1) significantly higher expected future free cash flows and 2) elevated trading multiples for those expected future free cash flows.

If you want to chat about any of this, we’re here to help: (713) 444-3560 or ctrimble@solycowealth.com.

No sooner than I put the Thanksgiving leftovers in the fridge than COVID rear its ugly, spiked head again and blew up Black Friday. Bah humbug, indeed. From an investor’s perspective, though, the timing, magnitude, and driver of last Friday’s volatility spike offer valuable lessons. Chief among these lessons are the benefits of:

No sooner than I put the Thanksgiving leftovers in the fridge than COVID rear its ugly, spiked head again and blew up Black Friday. Bah humbug, indeed. From an investor’s perspective, though, the timing, magnitude, and driver of last Friday’s volatility spike offer valuable lessons. Chief among these lessons are the benefits of: Each of Solyco Wealth’s four model investment portfolios outperformed its benchmark, net of fees, over the two-month period ending 11/8/21. As shown in the following table both the Aggressive and Moderately Aggressive portfolios, which hold heavier weightings to equities, also their first two months in existence exceeded returns for both the S&P 500 and the Russell 3000 after fees. Past performances are not indicative of future results, however.

Each of Solyco Wealth’s four model investment portfolios outperformed its benchmark, net of fees, over the two-month period ending 11/8/21. As shown in the following table both the Aggressive and Moderately Aggressive portfolios, which hold heavier weightings to equities, also their first two months in existence exceeded returns for both the S&P 500 and the Russell 3000 after fees. Past performances are not indicative of future results, however. As the 2021 holiday season quickly advances on us, now offers a sensible time to execute a quick run-through of a financial planning checklist. Just like with holiday shopping – which we also recommend you commence soon as supply chain issues likely will present challenges even greater than unraveling changes to the 2022 tax code – starting early probably leads to better outcomes. Here are a few quick pointers to get the ball rolling:

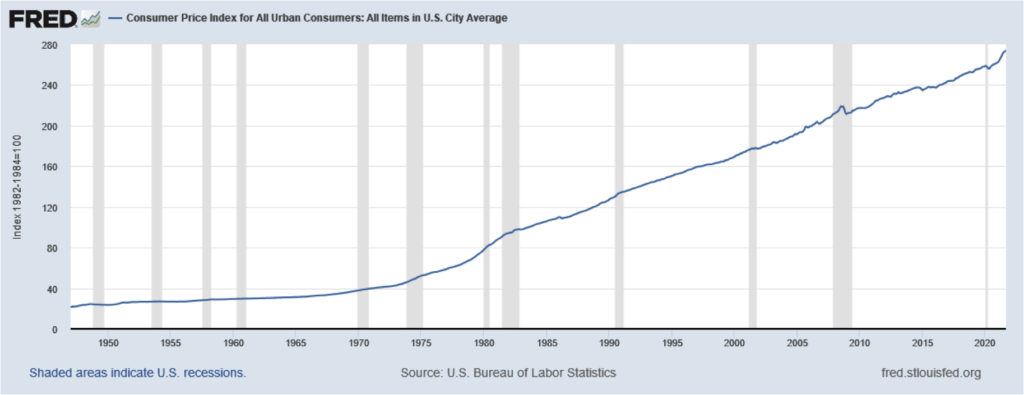

As the 2021 holiday season quickly advances on us, now offers a sensible time to execute a quick run-through of a financial planning checklist. Just like with holiday shopping – which we also recommend you commence soon as supply chain issues likely will present challenges even greater than unraveling changes to the 2022 tax code – starting early probably leads to better outcomes. Here are a few quick pointers to get the ball rolling: Inflation’s having a moment. Not since the hideous late-70s and early-80s has this economic phenomenon grabbed so many headlines. Many may not now be bothered by inflation like they weren’t by ‘70s fashion, but that seemingly little bend to the far right of the graph below likely represents $100s of dollars to even the stingiest households in higher costs for everything from Clorox bleach to Nikes to gasoline.

Inflation’s having a moment. Not since the hideous late-70s and early-80s has this economic phenomenon grabbed so many headlines. Many may not now be bothered by inflation like they weren’t by ‘70s fashion, but that seemingly little bend to the far right of the graph below likely represents $100s of dollars to even the stingiest households in higher costs for everything from Clorox bleach to Nikes to gasoline.

Earlier today the first bitcoin-linked exchange traded fund (ETF), ProShares Bitcoin Strategy (BITO), commenced trading on the New York Stock Exchange. I say “linked” as BITO doesn’t actually hold bitcoins. Rather, ProShares structured BITO as an investment vehicle in bitcoin futures, or contracts traded on the regulated Chicago Mercantile Exchange (CME) that track the future prices of bitcoins. I have no idea what ProShares’ “strategy” might be with respect to trading bitcoin futures other than simply being the first ETF to do so. While the first-mover advantage frequently represents a fine strategy, we’ll withhold judgment on this one for a while.

Earlier today the first bitcoin-linked exchange traded fund (ETF), ProShares Bitcoin Strategy (BITO), commenced trading on the New York Stock Exchange. I say “linked” as BITO doesn’t actually hold bitcoins. Rather, ProShares structured BITO as an investment vehicle in bitcoin futures, or contracts traded on the regulated Chicago Mercantile Exchange (CME) that track the future prices of bitcoins. I have no idea what ProShares’ “strategy” might be with respect to trading bitcoin futures other than simply being the first ETF to do so. While the first-mover advantage frequently represents a fine strategy, we’ll withhold judgment on this one for a while. The first month for Solyco Wealth’s Model Portfolios, which provide a risk tolerance-based framework for discussing client goals and investments, proved to be an eventful one. Characterized by ongoing debates concerning Fed policy, COVID impacts on labor supply, and the resulting impacts on domestic and international economies, the investing landscape offered plenty of challenges. All told, Solyco Wealth, which populates its model portfolios primarily with individual equities and fixed income exchange traded funds (ETFs), turned in a solid first month, as shown in the following table.

The first month for Solyco Wealth’s Model Portfolios, which provide a risk tolerance-based framework for discussing client goals and investments, proved to be an eventful one. Characterized by ongoing debates concerning Fed policy, COVID impacts on labor supply, and the resulting impacts on domestic and international economies, the investing landscape offered plenty of challenges. All told, Solyco Wealth, which populates its model portfolios primarily with individual equities and fixed income exchange traded funds (ETFs), turned in a solid first month, as shown in the following table. Asking great questions ranks as a superpower in my view. Doing so can elevate normal, everyday folks to exalted status. From “Can I help you with that box?” to “How’s your mother today?” to “Would you like fries with that?”, just having another human being display a modicum of concern frequently places a little more pep in a step or turns a frown upside down.

Asking great questions ranks as a superpower in my view. Doing so can elevate normal, everyday folks to exalted status. From “Can I help you with that box?” to “How’s your mother today?” to “Would you like fries with that?”, just having another human being display a modicum of concern frequently places a little more pep in a step or turns a frown upside down.  I get it: planning sucks. It’s like someone else always telling you what to do. Much of it involves trying to allocate insufficient resources to satisfy excess demand for those resources. Financial planning can be even worse: it involves money, which never seems to be oversupplied (unless you’re Elizabeth Warren bad-mouthing poor Jerome Powell). Undesirable terms like budget, taxes, required, beneficiary, and, yep, death, get thrown around ad nauseum (I threw Latin in there just to drive the discomfort point right where it needs to be).

I get it: planning sucks. It’s like someone else always telling you what to do. Much of it involves trying to allocate insufficient resources to satisfy excess demand for those resources. Financial planning can be even worse: it involves money, which never seems to be oversupplied (unless you’re Elizabeth Warren bad-mouthing poor Jerome Powell). Undesirable terms like budget, taxes, required, beneficiary, and, yep, death, get thrown around ad nauseum (I threw Latin in there just to drive the discomfort point right where it needs to be).  FedEx’s fiscal 1Q22 results, reported yesterday after market’s closed yesterday, may provide a snapshot of the U.S. economy. Earnings per share of $4.37 fell well short of the $4.92 S&P consensus estimate while revenue of $22.0 billion was in-line with the $21.9 billion consensus forecast. About ninety minutes before trading opens FDX shares traded $15.50, or 6.1%, lower at $236.57. Shares of FDX are not included in any accounts or model portfolios either personally or at Solyco Wealth. Also, I’ve got no view on FDX’s investability; I’m just using its results as an example of what potentially is going on across much of the U.S. economy and in the minds of management teams.

FedEx’s fiscal 1Q22 results, reported yesterday after market’s closed yesterday, may provide a snapshot of the U.S. economy. Earnings per share of $4.37 fell well short of the $4.92 S&P consensus estimate while revenue of $22.0 billion was in-line with the $21.9 billion consensus forecast. About ninety minutes before trading opens FDX shares traded $15.50, or 6.1%, lower at $236.57. Shares of FDX are not included in any accounts or model portfolios either personally or at Solyco Wealth. Also, I’ve got no view on FDX’s investability; I’m just using its results as an example of what potentially is going on across much of the U.S. economy and in the minds of management teams.