Emerging Market Debt and Junk Outperform Treasuries: What Gives?

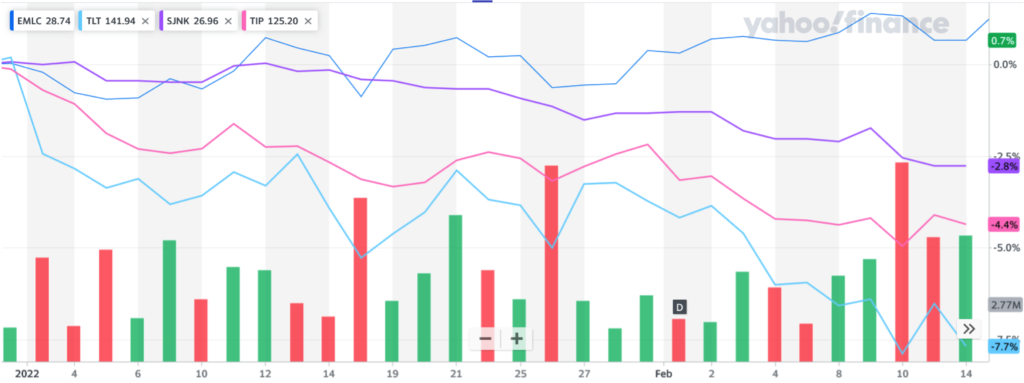

Exchange traded funds (ETFs) holding emerging market debt denominated in local currencies (EMLC in the graph below) – Brazilian reals, Chilean pesos, etc. – generally outperformed US long-term Treasuries (TLT) since the beginning of the year. Despite raging inflationary pressures, Treasury Inflation-Protected Securities (TIP) relative performance stinks. Junk bond ETFs (SJNK) performances’ also generally outpaced US investment-grade corporate securities since the beginning of the year. “What’s the fixed income world coming to?” one might ask.

Exchange traded funds (ETFs) holding emerging market debt denominated in local currencies (EMLC in the graph below) – Brazilian reals, Chilean pesos, etc. – generally outperformed US long-term Treasuries (TLT) since the beginning of the year. Despite raging inflationary pressures, Treasury Inflation-Protected Securities (TIP) relative performance stinks. Junk bond ETFs (SJNK) performances’ also generally outpaced US investment-grade corporate securities since the beginning of the year. “What’s the fixed income world coming to?” one might ask.

As usual, the devils reside in the details impacting these sectors of the fixed income markets. With respect to EMLC performance, the emerging market debt that trades in local currencies ETF, investment capital disproportionately flowed worldwide toward those economies that addressed inflationary pressures proactively: Brazil, Chile, and Mexico. Meanwhile, the US Fed’s inaction placed the domestic rate environment at a disadvantage vis-à-vis those more aggressive emerging markets governments.

Despite recent, 7% US inflation figures the TIP ETF declined 4.4% thus far in 2022. Differences in actual inflation and inflationary expectations largely explain this price decline. Investors commenced pricing expectations for higher domestic inflation into TIP late in 2021. From the end of 3Q21 to a peak price November 9, 2021, TIP appreciated 2.3% – a relatively large move for a fixed income ETF for such a short period of time. Notably, TIP’s recent 1.57% yield fell exactly in-line with iShares 1-3 Year Treasury Bond ETF’s yield, but the 1-3 Year ETF declined only 1% thus far in 2022. We conclude that TIP very rapidly priced in expectations for rising inflation late in 2021. Thus, barring a significant step-up for inflation expectations from 7% TIP appears relatively quite expensive.

The distinction between credit risk and rate risk defines the price performance discrepancy between SJNK and TLT. Investors estimate that the generally smaller and less well-capitalized companies that typically access the high-yield debt markets remain well-equipped to service their debt obligations. As such, these investors continue to purchase more SJNK, which offers a yield – 4.46% – almost three times higher than that of TLT (1.50%). It bears mentioning, though, that early 2022 total returns for SJNK and for TLT both were negative, however, due to their respective 2.8% and 7.7% price declines.

Since inception September 8, 2021, Solyco Wealth favored private credit providers Ares Capital (ARCC) and Hercules Capital (HTGC), over lower risk and lower yielding debt and credit investments. Both ARCC and HTGC maintain >70% of their loan portfolios in adjustable-rate debt. As a result, ARCC appreciated 2.1% and HTGC 7.3% thus far in 2022 while offering respective yields of 7.8% and 7.5%.