Why Downward Moves in Equity Markets Feel So Painful

Adages, aphorisms, sayings, and such gain popularity because they so often prove to be correct. A handful of my favorites:

Adages, aphorisms, sayings, and such gain popularity because they so often prove to be correct. A handful of my favorites:

- The market can remain irrational longer than you can remain liquid.

- This time it’s different.

- Bulls make money. Bears make money. Pigs get slaughtered.

- The market is a discounting mechanism.

With this missive I’ll focus on the last maxim: the stock market as a discounting mechanism. Equity markets in 2022 increasingly discount an impending recession. The drivers of this phenomenon range from supply shortages and logistical challenges driving outsized inflation to war, pollical strife and gridlock. Regardless of which of these factors most influences asset prices, their cumulative impact on sentiment probably exacts the most meaningful effect. The fact that negative sentiment commences to outpace fundamental factors really should not surprise investors, but it does so…repeatedly.

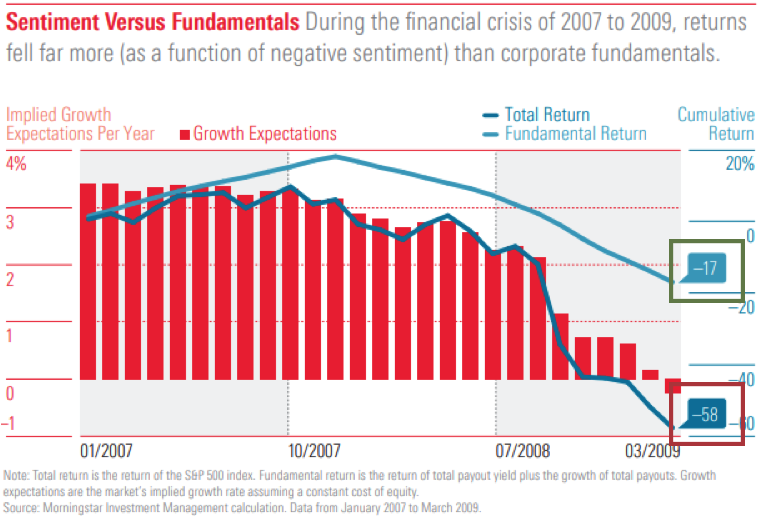

The following graphic from Morningstar details the degree to which the precipitous equity market downturn of 2007 to 2009 (black box) substantially outpaced the fundamentals of the S&P 500 (green box) over that period of time. While S&P 500 fundamentals deteriorated 17% over this period, the total return for the Index declined 58%!

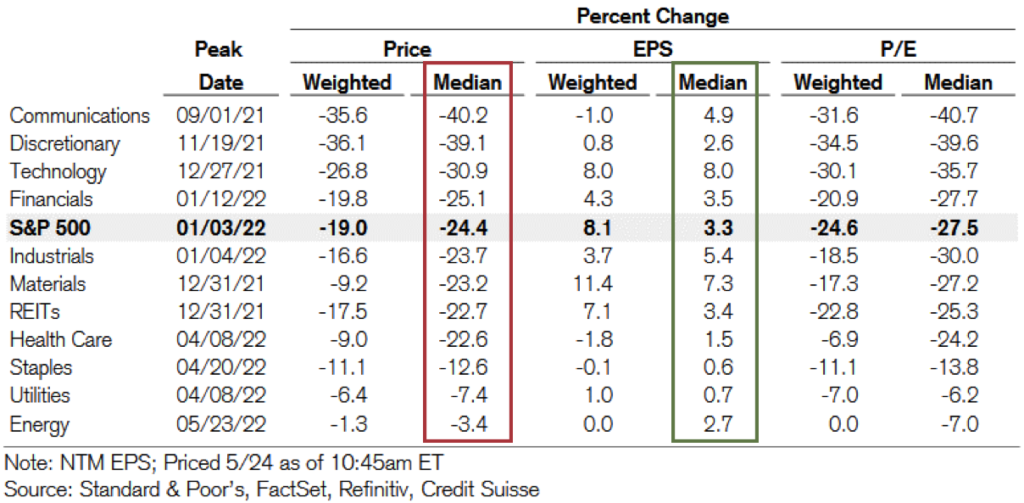

Recent research from Credit Suisse First Boston detailed a similar relationship between equity market activity to start 2022 and fundamentals (see following table). Whereas the median S&P 500 stock price dropped 24.4% since its peak level, S&P 500 earnings expectations increased 3.3%. The breadth of this expected earnings improvement remained broad as all eleven sectors posted improvements in their earnings prospects.

Obviously, the market discounts not earnings growth, but rather significant and painful earnings contraction. The massive money-making opportunity here exists in determining which discounting component is wrong: prices or earnings forecasts. My guess is that it will prove to be a little of both. As such, I prefer to err on the side of picking companies with more easily trackable earnings (Energy and Materials, for instance) and with large and established bases of operations (like Microsoft, ServiceNow, Cigna, and Humana).