A Yesteryear Name Focusing on Tomorrow: Old-School Tech

The 2022 wreck in Tech stocks, which declined ~19.8% as measured by the price change in Vanguard’s IT Index Fund (VGT), took a short reprieve yesterday (4/25/22). More share price pummeling commenced today (4/26/22), however, as one can see in the Yahoo! Finance chart below.

The 2022 wreck in Tech stocks, which declined ~19.8% as measured by the price change in Vanguard’s IT Index Fund (VGT), took a short reprieve yesterday (4/25/22). More share price pummeling commenced today (4/26/22), however, as one can see in the Yahoo! Finance chart below.

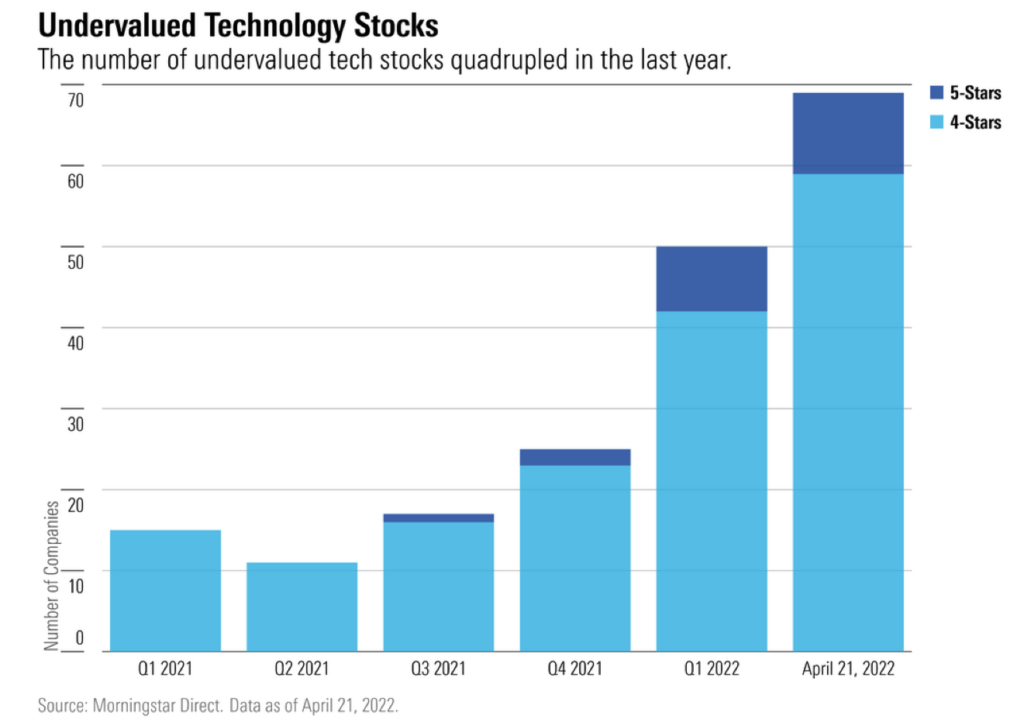

Much of this Tech stock price downdraft came amidst generally robust earnings and cash flow. In fact, the number of 4- and 5-star rated Tech stocks in Morningstar’s coverage universe, as reflected in the graph to the right, more than quadrupled from less than 20 for 1Q21 to almost 70 mid-week last week. Notably, that was before the acceleration of the price rout Friday, 4/22/22, and earlier this morning! Not known for being aggressive with its ratings and future estimates, such an increase in Morningstar’s highly rated Tech stocks obviously grabbed attention.

As I reviewed early 1Q22 earnings performances on Tech stock in particular also warranted interest: Corning (GLW). We neither advocate for buying to selling GLW shares, although we include them in our Conservative and Moderate Model Portfolios. Rather, we thought investors might be interested in a number of things about GLW. First, many may be surprised that the old-school glassmaker counts as a Tech stock. For 170 years, though, Corning’s been at the forefront of materials and glass technology counting cathode ray tubes for televisions, Gorilla Glass for iPhones, and fiber optics, among its inventions and improvements. Folks that buy and sell stocks irrespective of their industry classifications don’t care how S&P or whoever else categorizes companies by sector but doing so proves crucial in building and maintaining diversified portfolios.

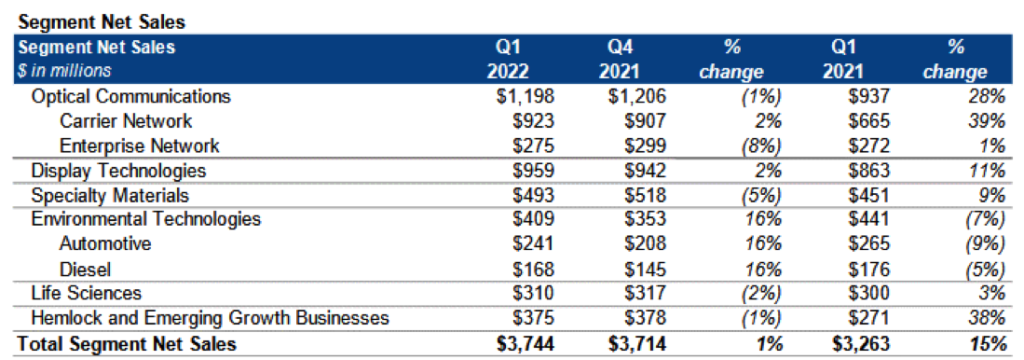

Second, by virtue of its creative applications of materials and glass technologies GLW built a very diverse set of end markets that not only benefits its financial performance and its investors, but also that yields solid observations on the state of these end markets. These observations, in our experience, often prove valuable for insights and conclusions for investments in Tech and other sectors. In its latest release of financial and operating results for 1Q22, for instance, GLW noted a 28% year-over-year increase in Optical Communications revenue. No guarantees here, but this significant increase could bode well for Telecom Equipment providers (Cisco, Arista Networks), cell-tower companies (American Tower, Crown-Castle SBA Communications), and/or enterprise cloud service providers (Microsoft, Amazon, Alphabet). Display Technologies also posted a double-digit, 11%, increase in sales for 1Q22 vs. 1Q21 with management specifically calling out positive exposure to Samsung’s Galaxy S22 Series smartphone. Maybe this indicates a little market share erosion for Apple: no way to tell for certain but it bears watching. Another interesting point on the diversity of GLW’s product portfolio that contributed to upside business results: Corning’s Life Sciences segment produced the vials from which 5.5 billion doses of COVID-19 vaccines were delivered.

Now, at this point, a discriminating investor might ask: “As the world hopefully won’t need 5.5 billion doses of any vaccines in the near future, won’t declines in this business hurt GLW’s future performance?” In response we anticipate that GLW’s management would reply that it expects the company’s Automotive segment, which saw revenue drop 9% from 1Q21 due to semiconductor availability and supply-chain issues, to more than make up for any loss in its Life Sciences segment. Just our guess, though. Anyway, here’s a breakdown of GLW’s 1Q22 sales by segment with prior period comparisons.